1

2

3

Authors:

Brenda J. Cude, Ph.D., NAIC Consumer Representative; Professor Emeritus, Department of

Financial Planning, Housing, and Consumer Economics, University of Georgia

Lisa Groshong, Ph.D.

Bonnie Burns, NAIC Consumer Representative

Acknowledgments and NAIC Disclaimer

Disclaimer: This study reflects the opinions of the authors and is the product of impartial research. It is

not intended to represent the positions or opinions of the NAIC or its members, nor are any of its contents

an official position of the NAIC or any of its members or staff. Any errors are the sole responsibility of the

authors.

Acknowledgments

The authors would like to thank the Financial Planning Association, a membership organization

for CERTIFIED FINANCIAL PLANNER™ professionals and those engaged in the financial planning process.

The FPA

promoted the opportunity to participate in the research through its existing

communications channels, which included newsletters, social channels, and chapter emails. We

would also like to thank the financial planners who participated in the interviews.

Suggested Citation

Cude, B. J., Groshong, L., & Burns, B. (2022).

Long-term care insurance rate increases and reduced benefit

options: Insights from interviews with financial planners. Center for Insurance Policy and Research (CIPR)

Research Report.

4

About the Center for Insurance Policy and Research

The National Association of Insurance Commissioners’ (NAIC) Center for Insurance Policy and Research

(CIPR) presents in-depth, independent research, the purposes of which are to: facilitate discussion and

advance thinking on insurance topics; promote action on current and emerging insurance issues; and

inform and disseminate ideas among regulators, consumers, academics, and financial services

professionals.

The above purposes are accomplished through the CIPR’s events, research publications, newsletter and

website, the Journal of Insurance Regulation, and extensive research library holdings.

CIPR studies are available at no cost on the CIPR website.

About the NAIC Consumer Representatives

The National Association of Insurance Commissioners’ (NAIC) Consumer Participation Program promotes

consumer representation and interaction with NAIC members by providing an opportunity for

individuals to participate in NAIC meetings, provided they represent consumer interests and meet

established criteria for appointment.

5

6

Table of Contents

Executive Summary ................................................................................................................................. 8

Introduction .......................................................................................................................................... 14

Background about Long-Term Care Insurance........................................................................................ 16

Traditional Standalone Long-Term Care Insurance Policies................................................................. 16

Rate Increases on Traditional Standalone Long-Term Care Insurance Policies .................................... 18

Reduced Benefits Options to Offset Rate Increases ............................................................................ 19

Research Methodology .......................................................................................................................... 20

Interviews with Financial Planners ..................................................................................................... 20

Data Analysis ..................................................................................................................................... 22

Emergent Themes from Interviews with Financial Planners ................................................................... 23

Financial Planner Perceptions of Client Motivation to Buy and Keep Long-Term Care Insurance ........ 23

Financial Security ........................................................................................................................... 24

Choice and Control ........................................................................................................................ 25

Concern for Family and Experience with Long-Term Care ............................................................... 25

Limited Options to Finance Long-Term Care without Current Policy ............................................... 26

Financial Planner Perceptions of Insurance Company Rate Increases, Reduced Benefit Options, and

Client Reactions to Them ................................................................................................................... 29

Some Rate Increases Should Have Been Avoidable......................................................................... 29

Rate Increase Notices Presented Basic Information Accurately, But the Information Was Inadequate

to Make a Decision ........................................................................................................................ 30

Notices May Create False Impressions or Undue Stress for Clients ................................................. 30

Clients Are Largely Unprepared to Make Decisions about Rate Increases ....................................... 31

Policyholders and Those Who Assist Them Need Additional Resources .......................................... 34

Financial Planner Advice to Clients about Rate Increases and Reduced Benefit Options ..................... 35

Keep the Policy with Its Current Benefits and Pay the Higher Premium .......................................... 35

If a Policyholder Must Choose a Reduced Benefit Option, Financial Planners Recommended

Dropping the Inflation Rider or Reducing the Benefit Period .......................................................... 36

Limitations ............................................................................................................................................ 37

Recommendations for State Insurance Regulators about Rate Increase Notices and Reduced Benefit

Options ................................................................................................................................................. 41

Recommendations for NAIC’s Long-Term Care Insurance Task Force ..................................................... 43

Conclusions ........................................................................................................................................... 45

References ............................................................................................................................................ 48

8

Long-Term Care Insurance Rate Increases and Reduced Benefit Options: Insights from

Interviews with Financial Planners

Executive Summary

As early as the 1970s, U.S. individuals and families could purchase long-term care

insurance to plan for future long-term care costs. While initially the policies primarily paid

benefits for nursing home care, those sold more recently cover other long-term care services,

for example, home health care. Today this type of long-term care insurance policy is frequently

described as traditional and standalone to distinguish it from newer hybrid policies that

combine long-term care coverage with other types of coverage, typically life insurance.

Many traditional long-term care insurance purchasers kept their policies, owning them

(and paying premiums) for decades. Now, many policyholders have received notices that their

premiums will increase, often dramatically. For example, media reports of premium increases

of 80% and even more than 100% are not uncommon.

The rate increase notices include choices for long-term care insurance policyholders to

consider that would offset part or all of the announced premium increase. These choices are

known as reduced benefit options and usually include reducing the maximum benefit period or

the daily, weekly, or monthly benefit amount. Policyholders also may be given the option to

reduce the maximum policy benefit to the total of past premiums paid (known as contingent

nonforfeiture) and pay no future premiums. Analyzing whether to reduce policy benefits and, if

so, which ones, or to pay a higher premium is a very complex choice for a typical policyholder,

especially without expert assistance.

9

Since 2020, the National Association of Insurance Commissioners’ (NAIC) Long-Term

Care Insurance (EX) Task Force has examined the issues surrounding reduced benefit options

and possible regulatory responses. Among its work products

1

are:

• An RBO Principles Document that gives guiding principles for regulators to communicate

to insurers regarding filing rate increase notices.

• Principles for Reduced Benefit Options (RBO) Associated with LTCI Rate Increases, which

offers recommendations to ensure that long-term care insurance policyholders have

opportunities to make reduced benefit decisions that are in their best interest.

• Checklist for Premium Increase Communications for state insurance department staff to

use when it reviews insurance company rate increase notices to consumers.

However, the NAIC has not attempted to directly examine consumer response to long-

term care insurance rate increase notices. This report describes a study that is a first step to fill

that gap. The report describes the major takeaways from interviews with 14 financial planners.

Interviews with financial planners are an indirect route to examine consumer responses to rate

increase notices. However, all of the financial planners had experience advising clients who had

received long-term care insurance rate increase notices that included reduced benefit options.

Following established qualitative research methodology, we identified three major

categories of themes from the interviews:

1

Available on NAIC’s Long-Term Care Insurance Task Force webpage.

10

• Financial planner perceptions of client motivations to buy and keep long-term

care insurance.

• Financial planner perceptions of insurance company rate increases, reduced

benefit options, and client reactions to them.

• Financial planner advice to clients about rate increase notices and reduced

benefit options.

Overall, we found that financial planners described client motivations to buy and keep

long-term care insurance as related to four major themes:

• Financial security, primarily related to preserving assets.

• Choice and control about the type and quality of long-term care they might

receive.

• Concern for family and experience with long-term care.

• Limited options to finance long-term care if they give up or reduce the benefits

of their current insurance policy.

Financial planner perceptions of insurance company rate increases and reduced benefit

options and client reactions to them related to five major themes:

• Some rate increases should have been avoidable, either because insurance

companies could have absorbed more, if not all, of the rate increases or because

state insurance regulators should have refused to approve rate increases.

• Rate increase notices presented basic information accurately, but the

information was inadequate to make a decision. For example, financial planner

11

clients said the notices did not include a satisfactory explanation as to why

premiums were increasing.

• Notices may create false impressions or undue stress for clients. Examples given

were notices that presented reduced benefit options as the client’s only options

rather than as examples or deadlines that created an unnecessary and false

sense of urgency.

• Clients were largely unprepared to make decisions about rate increases, lacking

contact with the agent who sold the policy, financial knowledge, and knowledge

about their own policy. The typical emotional response to a rate increase notice

made a rational decision more difficult.

• Policyholders and those who advise them need additional resources to assist in

making decisions.

Regarding the third category of themes from the interviews, financial planner advice to

clients about responding to a long-term care insurance rate increase notice, there were two

themes:

• Most financial planners advised their clients to keep their policies without

adjusting the benefits and pay the higher premium, if at all possible.

• When financial planners recommended accepting a reduced benefit option, it

was often either to drop the inflation rider or to reduce the benefit period.

12

The report concludes with recommendations for state insurance regulators and the

NAIC regarding rate increase notices and reduced benefit options. Key recommendations

include:

• State insurance regulators should fully use of NAIC’s Checklist for Premium

Increase Communications when reviewing long-term care insurance rate increase

notices.

• State insurance regulators should work to expand the advisors available to assist

policyholders with a decision about a long-term care insurance rate increase by:

o Requiring, by rule or regulation, that policyholders have the right to

authorize insurance companies to release policy information to a

professional advisor.

o Ensure that Senior Health Insurance Programs (SHIP) counselors are

prepared to advise long-term care insurance policyholders.

• NAIC should explore ways to facilitate the creation of smart disclosures to assist

policyholders in making decisions about reduced benefit options. For example,

with the input of personal information, the disclosure could narrow the choice of

reduced benefit options to those most relevant to the policyholder. The first step

for NAIC would be to identify what data would be needed, what data are

available, and whether those data are available in standardized, machine

readable form so they could be used to build interactive tools to assist

consumers.

13

• NAIC should revise its Checklist for Premium Increase Communication. The

research revealed revisions that would clarify whether reduced benefit options

in a rate increase notice are the policyholder’s only options or examples,

whether there is a firm deadline by which the policyholder must act, and the

consequences of dropping or adjusting inflation protection. We also recommend

adding two items to the checklist. One would encourage rate increase notices to

include a reminder to the policyholder to keep their policy in an easily accessible

location. A second recommended addition to the notices would remind

policyholders to identify a third party to be notified if premiums are not paid.

14

Introduction

As early as the 1970s, U.S. individuals and families could purchase long-term care

insurance to plan for future long-term care costs. Initially, the policies primarily paid benefits

for nursing home care if the policyholder met specific prescribed benefit triggers. With time,

long-term care insurance policies have extended the types of care covered to include other

long-term care services, for example, home health care. Today this type of policy is frequently

described as traditional and standalone to distinguish it from newer hybrid policies that

combine long-term care insurance with other types of coverage, typically life insurance.

Many traditional long-term care insurance purchasers kept their policies, now owning

them (and paying premiums) for decades. In fact, the lapse rate for traditional long-term care

insurance policies has been much lower than insurers anticipated when they first offered the

product.

Now, years after buying the policy and paying the same premium year after year, many

policyholders have received notices that the premiums for their long-term care insurance policy

will increase. Some have received multiple notices over time or notices of a current as well as a

future increase. Some of the premium increases are dramatic. For example, media reports of

premium increases of 80% and even more than 100% are common.

The rate increase notices include choices for long-term care insurance policyholders to

offset part or all of the announced premium increase. These choices are known as reduced

benefit options. The rate increase notices explain (in varying degrees of detail) policy benefits

that could be reduced and the impact of those reductions on future premiums. Policyholders

15

also may have the option to reduce the maximum policy benefit to the total of past premiums

paid (known as contingent nonforfeiture) and pay no future premiums. Analyzing whether to

reduce policy benefits and, if so, which ones or to pay a higher premium is a very complex

choice for a typical policyholder, especially without expert assistance.

In 2020, the National Association of Insurance Commissioners (NAIC) formed a Reduced

Benefit Options Subgroup within the Long-Term Care Insurance (EX) Task Force to examine

issues surrounding reduced benefit options and possible regulatory responses. Its charge was

to: Identify options to provide consumers with choices regarding modifications to long-term care

insurance (LTCI) contract benefits where policies are no longer affordable due to rate increases.

The Reduced Benefits Option Subgroup concluded its work in 2022. In 2020, it produced

an RBO Principles Document that gave guiding principles for regulators to communicate to

insurers regarding filing rate increase notices. The subgroup also created the document

Principles for Reduced Benefit Options (RBO) Associated with LTCI Rate Increases. The document

states that it is intended to answer this question: What are the recommendations for ensuring

long-term care insurance policyholders have maximized opportunity to make reduced benefit

decisions that are in their best interest? In 2021, in response to its charge, the subgroup

produced a Checklist for Premium Increase Communications, a document for state insurance

department staff to use when it reviews insurance company rate increase notices to

consumers. Finally, it created the document Issues Related to LTC Wellness Benefits to increase

clarity to regulators and industry regarding issues related to innovative long-term care wellness

programs. These resources are available on NAIC’s Long-Term Care Insurance Task Force

webpage.

16

However, the NAIC has not attempted to directly examine consumer response to long-

term care insurance rate increase notices. This report describes a study that is a first step to fill

that gap. The report describes the major takeaways from interviews with 14 financial planners.

Interviews with financial planners are an indirect route to examining consumer responses to

rate increase notices. However, all financial planners had experience advising clients who

received long-term care insurance rate increase notices that included reduced benefit options.

The report concludes with recommendations for state insurance regulators and the NAIC

regarding rate increase notices and reduced benefit options.

Background about Long-Term Care Insurance

Traditional Standalone Long-Term Care Insurance Policies

The NAIC’s (2019) Shopper’s Guide to Long-Term Care Insurance describes the policy

terms of a traditional standalone long-term care insurance policy. Two important policy terms

are the maximum benefit limit (commonly stated in years but sometimes as a total dollar

amount) and the daily/weekly/monthly benefit limit, typically stated as a dollar amount.

Neuhauser (2012) states that most traditional long-term care insurance policies treat coverage

as pooled coverage, defined as a multiple of the daily benefit amount and the benefit period.

Long-term care insurance policies have benefit triggers that determine eligibility to

receive benefits (NAIC, 2019). Insurers often use Activities of Daily Living (ADLs) as benefit

triggers. A common standard is being unable to do two of six (bathing, continence, dressing,

eating, toileting, and transferring) ADLs without human assistance for 90 days.

17

Traditional long-term care insurance policies also feature an elimination (or deductible)

period, stated as a number of days. Benefits begin at the end of the elimination period, which

may be counted in “calendar days” or “service days” (NAIC, 2019).

Traditional long-term care insurance policies also must offer inflation protection. With

automatic inflation protection, the benefit amounts go up automatically each year, typically by

a fixed percentage (often 3%) for a period of time (often 10 or 20 years). In a policy with special

offer inflation protection, the policyholder can choose to increase benefits from time to time. A

tax-qualified long-term care insurance policy offers certain federal income tax advantages,

specifically the opportunity for a taxpayer who itemizes deductions to deduct part or all of the

premium paid for the policy (NAIC, 2019).

Long-term care insurance companies medically underwrite coverage. Some companies

will not sell coverage to individuals with certain preexisting conditions or may charge those

individuals higher premiums (NAIC, 2019).

Cohen (2016) described the characteristics of an individual who bought long-term care

insurance by purchase year from 1990 to 2010. Over that period, the average purchaser age

decreased (from 68 years old in 1990 to 59 years old in 2010). The median income of a

purchaser dramatically increased – from $27,000 in 1990 to $87,500 in 2010. Purchasers also

were much more likely to be college educated and employed in 2010 than in 1990.

According to Cohen (2016), sales of traditional standalone long-term care insurance

policies peaked in 2003. In subsequent years, especially after 2010, sales of hybrid policies that

combine long-term care insurance with another insurance benefit, typically life insurance, have

18

outpaced those of traditional policies (Bodnar, 2016). The number of insurance companies

offering traditional policies has declined precipitously, from an estimated 125 in 2000 to fewer

than 15 by 2014 (Cohen, 2016). The U.S. Department of Treasury (2020) reported that the

downward trend in sales of traditional policies accelerated between 2014 and 2018.

Rate Increases on Traditional Standalone Long-Term Care Insurance Policies

In recent years, many policyholders with traditional standalone long-term care

insurance policies have received notices indicating their insurance premiums will increase,

often substantially. A report of a long-term care insurance data call to the NAIC Long-Term Care

Insurance Task Force (2021) described more than 3,500 approved rate increases nationwide for

long-term care insurance policies. The average single requested rate increase was 78%, while

the average single approved rate increase was 37%. The average cumulative approved rate

increase was 112%. The average policyholder attained age in the most rate increased

2

blocks

was 74.8 years old, ranging from 72.7 to 76.8 years old. Of the inforce policies in the most rate

increased blocks, more than 70% had an inflation rider and more than 35% had a lifetime

benefit period (Long-Term Care Group [LTCG], 2021).

Explanations for the rate increases typically are associated with the limited data on

which pricing assumptions for the product were based (U.S. Department of Treasury, 2020). A

consequence of the limited data was that insurance companies:

• Underestimated morbidity, or the number of policyholders who would need long-term

care and for how long;

2

Defined as the insurance company’s block with the largest past percentage rate increase (Personal

communication, Matthew Morton, November 18, 2022).

19

• Overestimated lapse rates, or the number of policyholders who would voluntarily drop

their policies.

The recent low-interest rate environment also has been cited as a reason for rate increases, as

the low interest rates reduced the income insurers earned against their assets (King, 2016).

3

The LTCG (2021) provided evidence that rate approval levels are inconsistent by state,

suggesting that policyholders in states where higher rates are approved subsidize policyholders

in other states. The report also concluded that “the cost of a nursing home does not appear to

be a primary predictor of state LTC experience” (Slide 3).

Reduced Benefits Options to Offset Rate Increases

Rate increase notices offer policyholders options to reduce policy benefits and offset

some or all of the announced premium increases. NAIC’s Model Long-Term Care Insurance

Regulation 641 (NAIC, 2017) states that at least one of the reduced benefit options must be

either a reduction in the maximum benefit or a reduction in the daily, weekly, or monthly

benefit amount.

NAIC’s (2020) Principles for Reduced Benefit Options (RBO) Associated with LTCI Rate

Increases described the most common reduced benefit options as:

• Reduce the daily benefit.

• Decrease the benefit period/maximum benefit pool.

• Reduce inflation protection going forward while preserving accumulated

inflation protection.

3

See King (2016) for an excellent explanation of the basics of pricing long-term care insurance.

20

• Increase the elimination period.

• Choose the contingent nonforfeiture benefit – Claim amount can be the sum of

past premiums paid. The policyholder only receives that benefit if they qualify

for a claim.

The less-common reduced benefit options mentioned in the same document were a cash

buyout and a co-pay percentage on benefits.

Thus, rate increases in the long-term care insurance market present significant

concerns. Long-term care insurance policyholders who receive rate increase notices must make

a complex decision about whether to keep the policy and pay higher premiums, reduce the

benefits and, if so, which ones, to offset some or all of the announced rate increase, or drop the

coverage. State insurance regulators must balance policyholder and insurer interests to

maintain the industry’s solvency while respecting the importance of a long-term care insurance

as part of an individual’s or family’s financial plan.

Research Methodology

Interviews with Financial Planners

In this project, qualitative data were collected via interviews with 14 key informants,

specifically financial planners who have worked with long-term care insurance policyholders.

We expected financial planners would understand not only the financial aspects of the long-

term care insurance policyholder experience but also the client’s complete financial plan.

The financial planners were recruited through the Financial Planning Association (FPA), a

membership organization for CERTIFIED FINANCIAL PLANNER™ professionals and those engaged in the

21

financial planning process. The FPA

promoted the opportunity to participate in the research

through its existing communications channels, which included newsletters, social channels, and

chapter emails.

The financial planners who were interested in participating in the research were asked

to complete an online survey. The questions in the survey were designed to ensure that those

selected had worked with clients who had long-term care insurance policyholders. We sought

financial planners who could answer yes to each of the following three screening questions:

• Have you regularly worked with long-term care insurance policyholders or people

requesting information about long-term care insurance?

• Have you commonly worked with long-term care insurance policyholders who received

a notice about a premium increase?

• Have you commonly worked with long-term care insurance policyholders who were

offered options to avoid a premium increase?

Fourteen financial planners met the criteria, and the second author scheduled

interviews. Twelve of the 14 completed an online survey that collected information about the

planners and their practices. The financial planners represented a mix of geographic regions,

including rural and urban locations, and males and females. Nine of the 12 planners had more

than 20 years of experience in the industry. All but one used a fee-based business model, with

fees typically based on Assets under Management; one financial planner’s practice was

commission-based. Ten of the 12 financial planners held the CERTIFIED FINANCIAL PLANNER™

designation; seven also were licensed insurance agents, and six held other professional

22

designations. Six planners said they worked with fewer than 50 clients, while five worked in a

firm that served 50 to 100 clients, and one worked in a firm with 500 to 1000 clients.

All but two financial planners provided their clients a range of financial planning

services, typically about estate planning, investments, insurance, retirement planning, and

taxes. Four focused on a specialized clientele, described as women, older adults, divorce

planning, and, in one case, long-term care planning. All of the financial planners indicated that

they followed a fiduciary standard.

The report’s first and second authors created a semi-structured script asking the

financial planners about their clients’ experiences with rate increases and reduced benefit

options. (See the appendix for the interview script.) The second author conducted the

interviews via Webex in October and December 2021 and January 2022.

4

On average, the

interviews were about 45 minutes to an hour. The researchers recorded each interview and

created a written transcript of each.

Data Analysis

The report’s first and second authors analyzed the transcripts independently using a

thematic content approach (Braun & Clarke, 2006) to identify nascent themes, identifying bits

of data that represented the themes across research participants. The second author and her

assistant coded the interview transcripts using NVivo analysis software (QSR International Pty.

4

The University of Georgia Institutional Review Board reviewed the project and classified it “Not Human Subjects

Research.”

23

Ltd.). The first and second authors then used the codes to develop higher-order themes

(Brower & Jeong, 2008), discussing and resolving interpretive disagreements.

Emergent Themes from Interviews with Financial Planners

We grouped the emergent themes from the interviews into three overall categories:

• Financial planner perceptions of client motivations to buy and keep long-term care

insurance.

• Financial planner perceptions of insurance company rate increases, reduced benefit

options, and client reactions to them.

• Financial planner advice to clients about responding to rate increase notices and

reduced benefit options.

Financial Planner Perceptions of Client Motivation to Buy and Keep Long-Term Care

Insurance

The interviews with financial planners confirmed what is already known about why

people bought traditional standalone long-term care insurance (Dorn et al., 2007; Grote, 2011).

Four major themes emerged related to financial planners’ perceptions of client motivations to

buy and keep long-term care insurance:

• Financial security.

• Choice and control.

• Concern for and experience with family members.

• Limited options to finance long-term care without their current insurance policy.

24

Financial Security

One theme was financial security. Financial security refers to clients’ desire to use

insurance to pay for long-term care if they need it while preserving their assets. As one financial

planner described it, they “just don’t want to spend their own money on long-term care.” The

financial planners grounded their observations about clients’ financial motivations in their

frequent descriptions of those who owned long-term care insurance policies as middle-class

consumers of moderate means when they bought their policies. One financial planner said,

“We had very, very modest people getting LTC. I remember the first policies we did … those

policies were dirt cheap, typically a thousand dollars (in premium a year) or less. And we could

give them to a much broader spectrum of clients.” For these individuals, financing long-term

care on their own might require using all of their assets.

Financial planners quickly observed that the financial situations of individuals buying

long-term care insurance today differ from those who bought policies decades ago. Today’s

long-term care insurance purchasers have higher incomes and net worth than purchasers in

previous decades. The planners often described the clients to whom they now recommended

long-term care insurance as having assets valued between $250,000 and $1 million. The

financial planners we interviewed said that clients with more than $3 to 5 million in assets can

self-insure. However, they noted that some high net worth clients might value long-term care

insurance as a way to preserve their estate or make care easier when navigating long-term care

services.

The change over time in the financial situation of long-term care insurance policyholders

is, in part, driven by an increase in long-term care insurance premiums. The NAIC has reported

25

that between 1990 and 2015, the average annual long-term care insurance premium more than

doubled (Papp, 2022).

Some financial planners mentioned gender as a critical consideration in the financial

motivation to buy and keep a long-term care insurance policy. One observed that women are

more likely to require long-term care support, and men are less likely to qualify for long-term

care insurance. Because women often outlive their husbands, they face the possibility of

spending down their assets to pay for the husband’s care, leaving nothing to support the

surviving spouse. One planner said, “I talk about the perils of self-funding (long-term care). And

particularly the perils for the wife. Usually, the wife is gonna be there to help take care of the

husband and she’s gonna outlive him. So what’s gonna happen to her? If they have to spend

money for his care, that’s gonna diminish the amount of assets.”

Choice and Control

Choice and control was another emergent theme related to financial planner

perceptions of client motivation to buy and keep long-term care insurance. Their clients want

alternatives to nursing homes and options enabling them to guide their own care. A financial

planner said, “The monetary thing is there, no doubt. But it’s really about maintaining a quality

end to your life.” One financial planner mentioned that news stories about conditions in nursing

homes during the pandemic had strengthened client resolve to keep the insurance policy they

have now, despite rate increases.

Concern for Family and Experience with Long-Term Care

An important motivation to buy and keep long-term care insurance was related to

concern for and experience with family members. Financial planners consistently reported that

26

clients saw insurance as a way to avoid becoming a burden on family. A financial planner

described one client who could self-insure but chose to buy insurance: “His statement to me

was ‘I don’t ever want to become a burden on any of my family members. I want to know that

there's an 800 number that I can have my niece or nephew or sibling contact and start

coordinating my care.’ He almost had a phobia about being burdensome, and yet he had so

much money.”

The financial planners also reported that experience with family members who needed

long-term care, especially for extended periods, as with Alzheimer’s disease and dementia,

5

motivated clients to buy and keep insurance. As one financial planner said, “It’s not because

they saw a commercial and thought, oh, that’s a good idea. I need some of that. It’s because

they lived it.”

Limited Options to Finance Long-Term Care without Current Policy

A motivation to keep an existing long-term care insurance policy was the lack of other

options to finance long-term care. Financial planners described it as “too late’” for

policyholders to apply for a new policy. The financial planners said clients who expressed an

interest in buying long-term care insurance at retirement age or later found it difficult to qualify

for coverage. “What we’re finding,” one financial planner said, “is that, particularly with my

clientele, they’re now above the optimal age to buy long-term care or have preexisting

conditions that would preclude them. You don’t buy long-term care with people in their

5

Coe et al.’s (2015) research confirms that family experience with long-term care influences the decision to

purchase insurance.

27

seventies, it's not viable.” Even if one could buy a new policy, it is doubtful that the premiums

would be less for coverage comparable to an existing policy.

One option that traditional long-term care insurance policyholders might consider is

replacing that policy with a hybrid policy. All of the financial planners we interviewed

mentioned hybrid policies. The financial planners were sharply divided in their opinions about

standalone policies versus hybrid policies.

Those who recommended hybrid policies to their clients typically mentioned three

reasons for their recommendations:

• Clients who want to purchase long-term care insurance could qualify for a hybrid policy

but not a traditional policy because of health conditions or age.

6

• Clients do not want to “waste” premiums if they never need to use the policy for long-

term care. A policyholder will get some value from a hybrid policy if only from the non-

long-term care aspect, typically life insurance. In this sense, hybrid policies also appeal

to clients with low risk tolerance. One financial planner described his response to clients

who did not want to “waste” premiums on a traditional standalone policy because they

might never use the coverage. He told them, “I would argue you would want to waste

your long-term care insurance premiums, because that means you had a long, healthy

life and you went quickly versus getting it dragged out.”

6

Braun et al. (2019) proposed that rejections are the main reason long-term care insurance take-up rates are less

than 10% among U.S. adults over age 62. Their model estimated that insurers would reject between 36% and 56%

of applicants for long-term care insurance between ages 55 and 66, the most common ages for application.

28

• Unlike a traditional long-term care insurance policy, financial planners said the rates for

a hybrid policy would never increase.

Nearly as many financial planners interviewed had misgivings about hybrid policies. The

primary reason they gave for their reservations about hybrid policies was that they were more

complicated than standalone policies. They thought a hybrid policy made it difficult for them

and their clients to be confident that they understood how and when the policy would pay

benefits as well as the policy’s value. Also, they described hybrid policies as generally only

available to clients with a substantial amount of cash on hand. One planner observed that

“most people don't have a hundred thousand dollars lying around that they can just plop into an

insurance policy. That's the problem with all these new products; they’re only designed for

people who have quite a bit of money rather than trying to design a product that everybody can

afford.”

Financial planners often described a mix of motivations that led to purchasing and/or

keeping a policy. For example, one financial planner’s description of their conversations with

clients touched on three themes: “Almost all … (were) either convinced that they could lose a

ton of money that they had built up through a long-term care event, or they had to have had

someone go through that in their family and recognized the need because they weren’t able to

pay for that care out of pocket or their family member had to go on Medicaid and then couldn’t

choose what facility to be in or choose to have at home care.”

29

Financial Planner Perceptions of Insurance Company Rate Increases, Reduced Benefit

Options, and Client Reactions to Them

Five major themes emerged related to financial planner perceptions of rate increases,

reduced benefit options, and client reactions to them:

• Some rate increases should have been avoidable.

• Rate increase notices presented basic information accurately, but the

information was inadequate to make a decision.

• Notices may create false impressions or undue stress for clients.

• Clients are largely unprepared to make decisions about rate increases, lacking

contact with the agent who sold the policy, financial knowledge, and knowledge

about their own policy. The typical emotional response to a rate increase notice

made a rational decision more difficult.

• Policyholders and those who advise them need additional resources to assist in

making decisions.

Some Rate Increases Should Have Been Avoidable

All of the financial planners’ clients who owned long-term care insurance policies had

received rate increase notices, especially those who had owned their policies for more than 10

years. Financial planners cited increases of up to 500%. Their experience is consistent with

other descriptions of rate increases (Darnell, 2021).

Some financial planners thought some rate increases should have been avoidable. They

said the carriers could and should have absorbed more, if not all, of the rate increases. One

30

said, “No one disputes rate hikes are a way of life, no matter what you’re buying, but this is way,

way outta control.”

Some financial planners thought state regulators should have done more to limit rate

increases. One financial planner said regulators justified allowing rate increases to keep insurers

in the market, “but they left anyway.”

Rate Increase Notices Presented Basic Information Accurately, But the Information Was

Inadequate to Make a Decision

The financial planners we interviewed described rate increase notices as presenting

basic information accurately. As one financial planner said, “The notices communicate that

rates are increasing. But they don’t necessarily help the client understand the reduced benefit

options to manage the premium.” One financial planner said she thought her clients “may

understand the communication … but not the repercussions” of the decision. Another said the

communications are not “broken down enough… as clients think in very simple non-insurance

terms.” Several planners also said clients want to know why premiums are increasing and the

notices do not explain that, at least not in a way their clients understand.

Notices May Create False Impressions or Undue Stress for Clients

Some financial planners thought some aspects of rate increase notices might create

false impressions or undue stress for clients. They thought some notices amplified the

policyholder’s emotional reaction by creating a false sense of urgency to make a decision. One

described the notices as “coming across as a drop-dead moment.” Some considered the

notices’ wording to be “enticements” to opt out of the policy and choose the contingent

31

nonforfeiture benefit for a paid-up policy. One financial planner said, “The first thing they (the

insurance companies) want to do is buy you out.”

Some financial planners questioned whether the options offered were in the company’s

best interest or the policyholder’s best interest and suggested that the two might not be the

same. One said that “the carrier has a vested interest in the policyholder’s decision regarding

lowering benefits.” Darnell (2021) supported this view, noting that policies may have large built-

in contract reserves to pay future benefits. Darnell suggests carriers have a vested interest in

policyholders reducing benefits because the carrier collects the decrease in the contract

reserve.

Several financial planners discussed the number of reduced benefit options mentioned

in the rate increase notice, asking questions such as “How many options are enough? How

many are too many?” They also commented that some notices list a limited number of options

and incorrectly imply those are the only options available to the policyholder.

Clients Are Largely Unprepared to Make Decisions about Rate Increases

Another theme in the financial planner interviews was that they believed their clients to

be largely unprepared to make decisions about rate increases. They gave several reasons to

support this observation. The financial planners said it was unlikely that policyholders were still

in contact with the agent who sold them the policy, either because the book of business was

sold or the agent was retired or deceased. Because the financial planners we interviewed had

not sold the policy to the client, they had limited access to policy information directly from the

insurance company. Some clients said they did not have a copy of the policy.

32

Financial planners typically characterized their clients as lacking the knowledge to

process the information about their options to reduce or avoid premium increases. The general

lack of financial literacy in the United States compounds the problem. For example, in 2022 the

FINRA Foundation reported empirical data that indicated that respondents with more financial

knowledge were more likely to exhibit positive financial behaviors, such as establishing an

emergency fund (Lin et al., 2022). However, only 36% demonstrated knowledge, indicating they

understood probabilities. On average, the respondents only correctly answered 2.58 of the five

financial knowledge questions (Urban & Valdes, 2022). In addition, the terminology and policy

benefits in long-term care insurance differ from those used in other insurance products, making

it more difficult for policyholders to understand their coverage.

Another financial planner reaction to rate increase notices referred to policies

purchased many years earlier. While a few financial planners said their clients expected rate

increases, most said their clients were resentful about the increases: “No one told me there

could be rate increases.” Even if the policyholder initially understood that rate increases were

possible, they likely have forgotten that information along with most of what they may have

known about the terms of their policy. Thus, unless the notice included at least a basic

description of the terms of the policy, the financial planners’ clients found it difficult to put the

options to reduce benefits into context.

Future premium increases are often predicted in the same multipage document. Thus,

policyholders may need help understanding both the immediate and the future implications of

choosing one reduced benefit option over another. For instance, a very large future premium

increase stated in the text may steer policyholders toward a paid-up option. Flexibility to

33

respond to possible future rate increases is another consideration. If a policyholder reduces a

daily benefit or maximum benefit period to the bare minimums to offset a rate increase, that

action likely limits or eliminates their options to respond to a future rate increase.

All of the financial planners described their clients’ emotional responses to a rate

increase notice. Often the emotional reaction was so strong it overwhelmed the client’s ability

to respond rationally. Financial planners said policyholders are often confused and angry, which

keeps them from focusing rationally on the issue. One financial planner said of their clients,

“They are just beside themselves with frustration.” Another described clients as “despairing.”

Another financial planner observation was about the emotional response to a rate

increase fueled by the perception of it as “sudden” after many years of paying the same

premium. The policyholders’ experience paying a “level” premium has reinforced their

perceptions that their premium would not increase. Policyholders contrasted the sudden

increase with the more incremental increase in other expenses over time. They also compared

the rate increase to their experience with other insurance products. One financial planner

added, “They knew that the cost of their life insurance didn’t go up and that the cost of some of

their other insurance products was guaranteed not to go up.” Also, their financial circumstances

have probably changed in the years since their initial purchase, sometimes because they have

retired and now live on a fixed income. Other policyholders may have experienced increases in

their assets’ value. Thus, a rate increase notice requires the policyholder to reevaluate their

financial plan to pay for long-term care, especially if their financial situation has changed since

they bought the policy. Their decision to buy long-term care insurance is something they would

prefer not to revisit.

34

Financial planners emphasized the importance of helping clients step back to look at the

rate increases and reduced benefit options rationally. A strong emotional response often clouds

judgment. One financial planner said he tries to approach such conversations with humor:

“What I do is turn around that anger and say, ‘Who is the dummy?’ They made a blanket bet on

people getting old and staying healthy or even taking their offer. They’re the ones that should

be angry because they’re the ones that made a bad business decision. You should be happy

because we made a good business decision.”

Policyholders and Those Who Assist Them Need Additional Resources

Regarding the final theme, financial planners seemed especially frustrated that their

clients could not ask the agent who sold the policy for assistance because the agent typically

was no longer associated with the insurance company. Because the financial planner had not

sold the policy, they said they could not access important information about the policy directly

from the insurance company.

Some financial planners thought that long-term care insurance companies should have

tools on their websites to explain rate increases and reduced benefit options. Others said their

clients do not use websites but thought financial planners would use online tools.

Several financial planners thought the ideal might be not to offer any options in the rate

increase notices but to encourage the consumer to talk with someone about their options. They

argued that the policyholder needs personalized advice to make a decision. Financial planners

said they consider the client’s personal situation when advising them about rate increases and

reduced benefit options. Client characteristics that often influenced financial planners’

35

recommendations were the client’s age and health; their financial assets, income, and net

worth; and their family medical and support history.

Financial Planner Advice to Clients about Rate Increases and Reduced Benefit Options

Two themes emerged regarding financial planner advice to clients in response to a rate

increase.

• Financial planners advised clients to keep the policy if at all possible and pay the higher

premium.

• If a client must choose a reduced benefit option to reduce the premium, financial

planners advise dropping the inflation rider or reducing the benefit period to offset

some of the rate increase and keep the policy.

Keep the Policy with Its Current Benefits and Pay the Higher Premium

All of the financial planners we interviewed recommended that their clients maintain

their long-term care insurance policy with its current benefits and pay the higher premium if

possible. Recall, however, that clients of financial planners are likely in a better financial

position to pay the higher premium than other long-term care insurance policyholders.

Reasons financial planners offered for their recommendation to keep the policy as is

included:

• The policy was likely underpriced from the beginning. However, policyholders may

not be swayed by this argument as they made their purchase decision based on

whether the premium at the time of purchase fit their budget then. It likely is not

36

helpful to tell a policyholder that they “should” have been paying a higher premium

earlier.

• If the policy has an inflation rider, the daily benefits have increased with time, and

the policy is worth much more now than it was initially.

• Most policyholders have limited options to replace the policy with another policy or

another approach to finance long-term care. Thus, keeping their existing coverage

may be their only option to use long-term care insurance to pay for care.

• The premium increase is likely small relative to the benefit, considering that some

policyholders are nearing the age where a claim is more likely. However true this

may be, it does not matter to a policyholder who cannot pay the higher premium or

would have to reduce their standard of living to pay it.

If a Policyholder Must Choose a Reduced Benefit Option, Financial Planners Recommended

Dropping the Inflation Rider or Reducing the Benefit Period

If a policyholder must choose a reduced benefit option rather than paying a higher

premium, financial planners typically recommended one of the following (depending on the

policy and the client’s situation):

• Drop the inflation rider or change the method from compound to simple. Financial

planners most often offered this advice if the client was older. The rationale was that

clients typically had held the policy for many years, and thus the daily benefit is now

generous due to annual inflation adjustments.

• Reduce the benefit period, especially if the daily benefit has increased due to an

inflation rider. A few financial planners described the benefit of this approach when

37

benefits are pooled. For example, suppose one client has a $100 daily benefit for four

years – that is access to $146,000 in benefits. Another client has a $200 daily benefit for

two years – also access to $146,000 in benefits. But, the second client would not have to

pay any of the covered costs out of pocket for the first two years on claim after the

elimination period as long as the daily cost is less than $200. Moreover, he can “bank”

the difference to functionally extend the benefit period.

Both recommendations are consistent with those of respected financial planning

authorities such as Kitces (2013). Nawrocki (2012) also suggested that maintaining an insurance

policy, even with fewer benefits, would still give policyholders access to services that a policy

might include, such as care coordination.

None of the financial planners said they would advise their clients to drop the policy.

However, a few did say they would consider different options if their client’s assets have

decreased since they bought the policy to, for example, delay using Medicaid. Some said they

discussed other ways to supplement their clients’ long-term care insurance benefits. For

example, they might discuss a cash value life insurance policy or a reverse mortgage, especially

if the client chooses to reduce their policy’s daily benefit or maximum benefit period.

Limitations

It is important to state that we do not think that what we learned from the financial

planners is universally applicable to long-term care insurance policyholders. Because this was

qualitative research, the results cannot be generalized to all clients of financial planners or all

long-term care insurance policyholders.

38

In addition, there are two important caveats related to learning about long-term care

insurance policyholders’ experiences by interviewing financial planners:

• Financial planners’ clients likely have more assets than some other long-term care

insurance policyholders. Thus, they likely have more options to not only pay a rate

increase but also to finance long-term care using other financial resources.

• It seems likely that clients of financial planners would assume their financial planner

could advise them about their response to the rate increase. Other long-term care

insurance policyholders may not have a relationship with a professional from whom

they could seek advice about this decision. For example, if their personal insurance

agent (for homeowners and auto insurance, perhaps) does not sell long-term care

insurance, it is unlikely they are qualified to offer advice. Thus, policyholders who do not

work with a professional advisor may approach the decision differently than those who

do, and some may ignore the rate increase notice.

In a September 21, 2020, letter to the NAIC’s Long-Term Care Insurance Reduced

Benefits Options Subgroup, Bonnie Burns, a nationally-known expert on long-term care

insurance and a co-author of this study, highlighted several ways in which the reactions of a

policyholder who does not consult a professional will likely be similar to and differ from those

the financial planners described. She wrote:

• Policyholders of advanced age have difficulty processing complex choices and often fail

to act. Notices that run to multiple pages with dense text and boxes are difficult for

many older and sometimes even younger readers to interpret.

39

• Policyholders, and sometimes family members, react in frustration by stating they will

just cancel the policy. This fairly frequent reaction is often in response to a very large

rate increase, and an individual being overwhelmed by the density of the language and

the mysterious choices in a multipage notice.

• Policyholders who did not respond to a notice will sometimes ask for help after

premiums have increased for several months and have had a noticeable effect on their

budget. People who pay quarterly or semi-annually may simply stop paying an

unaffordable premium. Family members are often not aware that this has occurred until

later.

• Family members acting on behalf of an elderly family member have little understanding

of long-term care insurance or the relative value of each option offered, and will look for

the option with the most premium reduction: “the most bang for the buck.” That option

is often the elimination of inflation protection without understanding the effect on

future or past benefits.

• Family members sometimes act on behalf of an elderly relative, often very late in the

process or after a deadline, when the policyholder may have fewer choices to reduce

the impact of an increased premium.

• Many policyholders have premiums set up as “auto pay,” a process that is difficult to

change or turn off and complicates discussions about reductions or changes in premium

payments.

40

• Family members often ask for help after a policyholder has made a decision that is not

in their best interest, with varying responses from insurers willing to make adjustments

to those prior decisions.

• Family members and policyholders often react to explanations about the reason for an

increase by asking why they are paying for the mistakes an insurer has made. They

believe they are paying to maintain the insurer’s profitability, and are skeptical of

explanations to the contrary.

• Policyholders and others tend to miss important information that is not immediately

obvious, such as the likelihood of future rate increases or an increase that is spread over

several years. This is sometimes because the placement of this information is in a long

paragraph of information or explanation.

Other limitations of the study are identified below.

• Most of the financial planners we interviewed were not familiar with partnership

policies. Consequently, this research provides no insights into reduced benefit options

for partnership policies, which help the policyholder manage the financial impact of

spending down assets to meet Medicaid eligibility standards (NAIC, 2019).

• We did not discuss with the financial planners that we interviewed the long-term care

insurance policies in the closed block administered by Senior Health Insurance of

Pennsylvania (SHIP). Nor did we discuss policies impacted by class action lawsuits;

decisions about rate increases and reduced benefit options for these policies are likely

more complicated than those discussed in our financial planner interviews.

41

This research also did not attempt to assess the impact of any of the work of the NAIC’s

Reduced Benefit Options Subgroup. Research with that goal in mind likely would require an

experimental approach. For example, researchers could give long-term care insurance

policyholders a rate increase notice at two points in time: before a state insurance regulator

has reviewed it using the Checklist for Premium Increase Communications and after.

Researchers could then compare policyholder understanding of the information in the two

notices.

Recommendations for State Insurance Regulators about Rate Increase

Notices and Reduced Benefit Options

We recommend the following actions for state insurance regulators regarding long-term

care insurance rate increase notices and reduced benefit options:

• Make full use of NAIC’s Checklist for Premium Increase Communications (NAIC, 2021)

when reviewing rate increase notices. The checklist offers many criteria that, if followed,

would lead to improved communication with policyholders. For example, one item in

the checklist states specifically that communications should “present options fairly and

without subtle coercion.” Another item is, “Are the options represented fairly? Options

are not presented fairly if one option is emphasized, mentioned multiple times, placed

in a more prominent position, or bolded when the other options are not.” A third reads,

“Are the number of options presented reasonable? If there are more than 5, engage

with insurer to understand what is being presented.” Given the financial planners’

concerns about how rate increase notices present reduced benefit options, attention to

that aspect of the notice seems essential.

42

How reduced benefit options are presented also influences policyholder

understanding of the information. For example, it may be unclear when the policyholder

can change any of the terms of their policy, not just the terms presented in the notice.

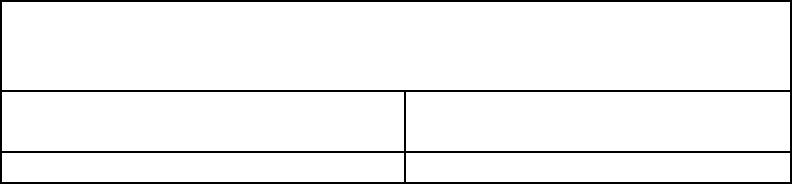

Wording such as the following illustrates a way to emphasize when reduced benefit

options in the notice are merely examples:

You have options to reduce your new premium. Here is one example.

If you’re comfortable changing your benefits from lifetime coverage to six

years of benefits, your new premium will be lower. The rest of your benefits

will stay the same.

Your premium today for unlimited

benefits

Your premium for 6 years of benefits

$9,000 annually

$7,000 annually

Here is another example……

You can call customer service at 800-000-0000 to ask about other changes you

can make to reduce the new premium.

The concrete example in the table helps the policyholder contextualize the information.

Note that the example also includes the original policy benefits, information the

policyholder may not have readily available.

• State insurance regulators should work to expand the advisors available to assist

policyholders with a decision about a long-term care insurance rate increase. Ultimately,

the financial planners suggested that a decision about reduced benefit options is so

complex that counseling is required to assist the policyholder. One recent report

suggested that more Americans turn to family and friends (56%) and prayer (29%) than

to a professional (27%) for financial advice (Nationwide, 2022). While family and friends

43

may be supportive and prayer comforting, consumers need advice from objective

professionals to assist them in making sound decisions.

The financial planners reported that it is rare that the agent who initially sold the

long-term care insurance policy is available. Other experts (other insurance agents,

financial planners, attorneys) could advise long-term care insurance policyholders. But

they often cannot get information about the policy from the insurance company,

information they would need to be truly helpful to the policyholder. Nor may an

insurance agent who writes, for example, auto insurance coverage, have any expertise

to assist a policyholder with a decision about long-term care insurance.

States can take two actions to expand the scope of advisors available to assist

consumers. One is to ensure, by rule or regulation, that policyholders have the right to

authorize insurance companies to release policy information to a professional advisor.

Another way that states can expand the scope of advisors is to ensure that

Senior Health Insurance Program (SHIP) counselors are prepared to advise long-term

care insurance policyholders. In two-thirds of the states, SHIP counselors are located in

agencies other than Departments of Insurance. Departments of Insurance should open

the lines of communication with those agencies and partner to provide training as well

as standby technical assistance to the SHIP counselors.

Recommendations for NAIC’s Long-Term Care Insurance Task Force

We have two recommendations for NAIC’s Long-Term Care Insurance Task Force. The

first is to explore (perhaps in coordination with NAIC’s Cybersecurity, Innovation, and

Technology (H) Committee) ways to facilitate the creation of smart disclosures to assist

44

policyholders in making decisions about reduced benefit options. For example, with the input of

personal information, the disclosure could narrow the choice of reduced benefit options to

those most relevant to the policyholder. In a very simple example, a smart disclosure might

provide the cost of care where the policyholder would seek that care. The tool then could

indicate how that cost compares to the policyholder’s daily benefit and, if it compares

favorably, suggest evaluating an option to reduce the benefit period. Alternatively, a smart

disclosure might suggest whether to consider dropping inflation protection based on the

policyholder’s age and current benefit amount. Ultimately, the policyholder would still have to

make the decision but could have tailored information to narrow the choices to those most

applicable to their situation. The first step for NAIC would be to identify what data would be

needed, what data are available, and whether those data are available in standardized,

machine readable form so they could be used to build interactive tools to assist consumers.

A second recommendation is to use the knowledge generated by this research to

improve NAIC’s Checklist for Premium Increase Communications. The checklist is organized into

12 sections. The phrases in bold below refer to those sections; numbers refer to checklist items.

• Revise the Readability and Accessibility #15 item to read: Are there side-by-side

illustrations showing how the RBOs impact the policy benefits and premiums?

• Revise the Identification #19 item to read: Does the communication clearly indicate its

purpose is to inform the consumer of a rate increase?

• Add an item to Identification #23 -- Does the communication clearly indicate whether

the RBOs listed are the policyholder’s only options or if they are examples of options? If

the identified RBOs are examples, then they should be clearly described as such

45

throughout the communication. If the identified RBOs are examples, does the

communication clearly indicate how the policyholder can learn about other options?

• Add to the Identification #24 item: Does the communication make it clear if there is a

deadline to elect an option? If there is no deadline, the communication should avoid

creating a false sense of urgency to act.

• Revise the Consultation and Contact Information item #35 to add "someone who could

advise as to the impact on eligibility for public benefits."

• Revise the Understanding Options - Impact of Decisions item #54 to read: Does the

notice include a declarative statement about whether dropping or adjusting inflation

protection results in the loss of some or all of the accumulated benefit amount?

• Add: Does the notice include a reminder to the policyholder to keep the notice and

attach it to the policyholder's long-term care insurance policy? Does the notice

encourage the policyholder to keep the policy and related documents in an easily-

accessible location (not in a safe deposit box) and inform the appropriate individuals

about where the policy can be found?

• Add: Does the notice include a reminder that the policyholder can identify a third party

to be notified if premiums aren't paid and information about how to make that

election?

Conclusions

Rate increases on long-term care insurance policies threaten the financial security of

individuals and families who plan to rely on them to help with the cost of their future care. The

rate increases also further undermine Americans’ trust in the insurance industry.

46

In this study, we interviewed 14 financial planners who had worked with clients who

had received at least one notice of a rate increase on their long-term care insurance policies.

Overall, we found that financial planners believed policyholders were largely unprepared to

make decisions about rate increases. While the insurance company notices may have presented

basic information about the rate increase, they did not, and perhaps cannot, present all of the

information needed to decide whether to retain the policy as is or choose a reduced benefit

option to offset at least some of a premium increase. The decision requires a thorough

evaluation of the policyholder’s age and health; financial assets, income, and net worth; and

family medical and support history. Policyholders typically lack the knowledge to make such a

complex evaluation independently.

State insurance regulators can help policyholders in two ways that would expand the

scope of advisors available to help them with a long-term care insurance decision. One is to

ensure, by rule or regulation, that the policyholder can authorize the insurance company to

release policy-specific information to a designated professional advisor. This authorization is

essential because the insurance agent who sold the policy is usually no longer affiliated with the

company and cannot assist the policyholder. Another action state insurance regulators can take

is to ensure that State Health Insurance Program (SHIP) counselors are prepared to advise long-

term care insurance policyholders. In states where SHIPs are located in agencies other than the

Department of Insurance, Departments of Insurance should provide training and standby

technical assistance to SHIP counselors.

NAIC’s Long-Term Care Insurance Task Force can explore (perhaps in coordination with

NAIC’s Cybersecurity, Innovation, and Technology (H) Committee) ways to facilitate the

47

creation of smart disclosures to assist policyholders as they make decisions about reduced

benefit options. For example, a policyholder could enter information into the smart disclosure

that could tailor available reduced benefit options to the policyholder’s personal situation.

Personalizing the reduced benefit options to those most relevant to the policyholder would

reduce the complexity of the decision.

The research also suggests improvements to NAIC’s Checklist for Premium Increase

Communications. The revisions we recommend would create greater clarity in several areas.

One is to clarify whether reduced benefit options in a rate increase notice are the policyholder’s

only options or examples. Another is whether there is a firm deadline by which the policyholder

must act. A third is the consequences of dropping or adjusting inflation protection. We also

recommend adding two items to the checklist. One would encourage rate increase notices to

include a reminder to the policyholder to keep their policy in an easily accessible location. A

second would encourage a reminder to the policyholder to identify a third party to be notified if

premiums are not paid.

48

References

Bodnar, V. (2016, May). Insurer in-force long-term care insurance management. In The state of

long-term care insurance: The market, challenges, and future innovations. National

Association of Insurance Commissioners and the Center for Insurance Policy and

Research. https://content.naic.org/sites/default/files/inline-

files/cipr_current_study_160519_ltc_insurance_0.pdf

Braun, R. A., Kopecky, K. A., & Koreshkova, T. (2019). Old, frail, and uninsured: Accounting for

features of the U.S. long-term care insurance market. Econometrica, 87(3), 981-1019.

https://doi.org/10.3982/ECTA15295

Braun, V., & Clarke, V. (2006). Using thematic analysis in psychology. Qualitative Research in

Psychology, 3(2), 77-106. https://doi.org/10.1191/1478088706qp063oa

Brower, R. S., & Jeong, H.-S. (2008). Grounded analysis: Going beyond description to derive

theory from qualitative data. In S. Brandler, C. R. Roman, G. J. Miller, & K. Yang (Eds.),

Handbook of research methods in public administration (pp. 823-839). Taylor & Francis

Group.

Coe, N. B., Skira, M. M., & Van Houtven, C. H. (2015). Long-term care insurance: Does

experience matter. Journal of Health Economics, 40, 122-131.

https://doi.org/10.1016/j.jhealeco.2015.01.001

Cohen, M. A. (2016, May). The state of the long-term care insurance market. In The State of

long-term care insurance: The market, challenges, and future innovations. National

Association of Insurance Commissioners and the Center for Insurance Policy and

Research. https://content.naic.org/sites/default/files/inline-

files/cipr_current_study_160519_ltc_insurance_0.pdf

Darnell, R. W. (2021, June). Long-term care and actuarial equivalence. Long-Term Care News.

https://www.soa.org/sections/long-term-care/long-term-care-newsletter/2021/june/ltc-2021-06-darnell/

Dorn, M. E., Sharpe, D. L., Dickey, G., & Herring, D. D. (2007). Understanding the determinants

of a long-term care insurance purchase. Journal of Financial Planning, 30(11), 38-46.

Grote, J. (2011, May). Keeping ahead of the long-term care domino. Journal of Financial

Planning, 24(5), 22-28.

King, E. (2016, November). Long-term care insurance pricing basics. CIPR Newsletter, pp. 11-13.

Kitces, M. E. (2013, April). 5 ways to handle a long-term-care insurance rate increase. Journal of

Financial Planning, 26(4), 26-29.

Lin, J. T., Bumcrot, C., Mottola, G., Valdes, O., Ganem, R., Kieffer, C., Lusardi, A., & Walsh, G.

(2022). Financial capability in the U.S.: Highlights from the FINRA Foundation National

Financial Capability Study (5

th

Ed). FINRA Investor Education Foundation.

https://finrafoundation.org/sites/finrafoundation/files/NFCS-Report-Fifth-Edition-July-

2022.pdf

49

Long-Term Care Group, Inc. (2021, June 25). NAIC LTC data call Workstream #6 suggested public